An important point for members of the FI industry to acknowledge is that they are not in the business of providing financial services and products; they are in the business of providing customer experience.

If they don’t already think this way, they should.

Customer expectations for every organization in every industry have changed and the FI industry is not immune to these expectations.

It’s no longer bank vs. bank in the consumer’s eye either.

They are judging the customer experiences they have with FI organizations against the customer experiences they have with organizations from all industries—companies including digital trailblazers like Apple, eBay, PayPal, Google and more.

Perhaps this is why, as revealed in a recent Celent survey, for the first time ever, sales was not the top priority for banking executives—improving customer relationships was.

Source: Celent

So how can FI organizations deliver a better customer experience? By undergoing a digital transformation.

The benefit of digital transformation

Today’s consumer expects their dealings with an FI organization to be fast, easy and seamless no matter what channel they are using. Undergoing a digital transformation will allow FI organizations to do this and enhance the customer experience they’re providing at every touchpoint of the customer journey.

So what’s holding banks back?

While, as the survey mentioned above indicates, many FI institutions recognize that digital transformation is critical to executing their strategy and delivering future growth, many are dragging their heels.

Consider this quote made by Peter Sands, former Group CEO of Standard Chartered PLC.

“Banking is very digitisable, but we have not yet seen the fundamental transformation of business models that have taken place in other sectors. Margins will fall unless banks reinvent what they offer and how they work.”

Pretty profound statement for today’s FI community to digest. The irony is Peter made that statement back in the summer of 2013!

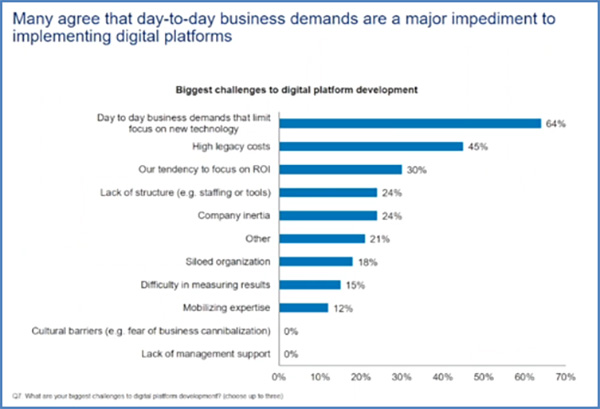

So what’s holding FI organizations back from embracing digital transformation? 64% of bank executives surveyed said the biggest impediment is day-to-day business demands that limit the amount of time personnel can spend on implementing their digital strategy.

Source: Celent

The commitment has to start at the top

The most important thing that needs to happen if an FI organization’s digital transformation is going to be successful is C-level buy-in.

C-level backing is crucial if digital transformation is going to take place. Without it, digital transformation will be difficult because the transformation has to occur throughout the organization.

Everyone must be onboard. Remember the point of digital transformation is so the organization can create an omni-channel customer experience that is consistent at every touchpoint of the customer journey.

It takes a framework

In order to deliver a customized but consistent FI brand experience to customers across all channels and points of interaction, transformation to digital banking requires a framework.

This framework must be underpinned by analytics and automation. To accomplish this it will require a change in products and services, IT, personnel and the organization as a whole. Following this framework will be key to delivering economic value that is demonstrable and sustainable.

Enhance the customer experience and other metrics will improve as well

The transformation to digital needs to be more than a customer retention strategy in order to justify the scale and frequency of investment. It must also generate profit, which it will in three ways:

- Revenue Uplift: The revenue pool will be stabilized or increased because of increased customer satisfaction and retention, interaction and penetration; customized pricing, and new products providing new revenue streams.

- Risk Cost Mitigation: Decision making and portfolio management will be more informed which will lead to lower credit losses, reduced fraud costs and optimized liquidity.

- Operational Cost Reduction: The operational cost base will be stabilized or even shrink driven by the redesign of the branch network, lower transaction and service costs and the streamlining of regulatory reporting.

Can digital transformation really make a difference?

The answer is “Yes”.

Recently Quadient was engaged by the Bank of Montreal to execute a digital transformation assignment.

The project was a digital onboarding of the personal banking experience, via mobile banking. BMO wanted to improve the customer experience and drive efficiencies associated with the current process.

The goal was to standardize and improve the process automation that ultimately opened the access to e-form and e-signature capabilities.

When the project was completed, customers were able to set up a bank account via a smartphone device in less than eight minutes, with paper forms completely eliminated from the process.

- BMO has enjoyed a very healthy ROI from this project.

- More satisfying and convenient customer experience

- Revenues have increased up to $12 million

- 80% reduction in errors and irregularities

- 40% improvement in process efficiencies

- Elimination of all paper forms—2.3 MM sheets of paper

- Reduction of paper will save BMO $321 million per year

- Digital adoption across 940 retail branches in Canada

Learn how you can increase sales by making the customer experience your organization’s first priority. Watch the webinar “Using Digital Transformation to Deliver a Better Customer Experience”.

You can also read the Celent Case Study - BMO: Digital Transformation in Personal Banking.

Andrew Stevens leads Quadient’s global enterprise digital product marketing team. Andrew is a recognized expert at all levels of enterprise IT, supplier, and process management, with 25 plus years’ experience leading global teams in areas including cross-boundary governance, architectural analysis, portfolio strategy and solutions development through to live support. Andrew specializes in helping enterprises optimize their communication and experience solutions to deliver the highest levels of accuracy while continuing to deliver great customer and business outcomes.