Days Sales Outstanding (DSO): What is it, Formula, & How to Improve it?

Nicole Dwyer

September 5, 2023

6 Minutes

In this blog, you'll find

What is DSO?

Days sales outstanding (DSO) is the average number of days that receivables remain outstanding before cash is collected. This number shows the speed of cash flow, and provides an indicator of the efficiency and profitability of the business.

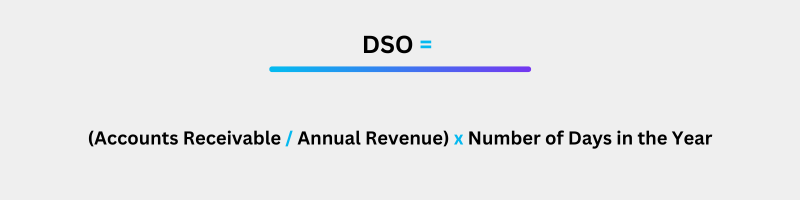

How to calculate DSO?

The calculation for DSO is:

(Accounts receivable ÷ Annual revenue) × Number of days in the year

For example, let’s say we have a retail business with $70,000 in their AR balance sheet, and an annual revenue of $1,000,000. The formula would be:

($70,000 / 1,000,000) x 365 = 25.5 days for DSO

This tells us that it typically takes that retail business 25 days to collect cash for its invoices.

DSO Calculator

@media screen and (max-width: 640px){#og_iframe{height: 620px;width:100%;}}@media screen and (min-width: 641px) and (max-width: 1024px){#og_iframe{height: 620px;width:100%;}}@media screen and (min-width: 1025px){#og_iframe{height: 620px;width:100%;}}

Why is DSO important?

DSO is a metric CFOs and CEOs will look at to evaluate if the company's credit and collection efforts are effective. On an overall level, it shows how quickly a company can reinvest cash into its own business for continued sales and potential growth. Following DSO trends for the business over time, executives can see if the business is becoming more or less efficient over time, if credit or collections policies need to be adjusted, or how economic conditions are impacting the health of the business.

AR teams also use DSO, not just for broader business trends, but also at the individual customer level. Tracking this allows them to see if a customer is experiencing cash flow issues that might impact the business and the relationship overall. This might lead to changes in credit and payment terms extended to individual customers, and how AR teams choose to segment customers for such terms.

Featured Resource:

The Essential Guide to Day Sales Outstanding

What's a “good” DSO number?

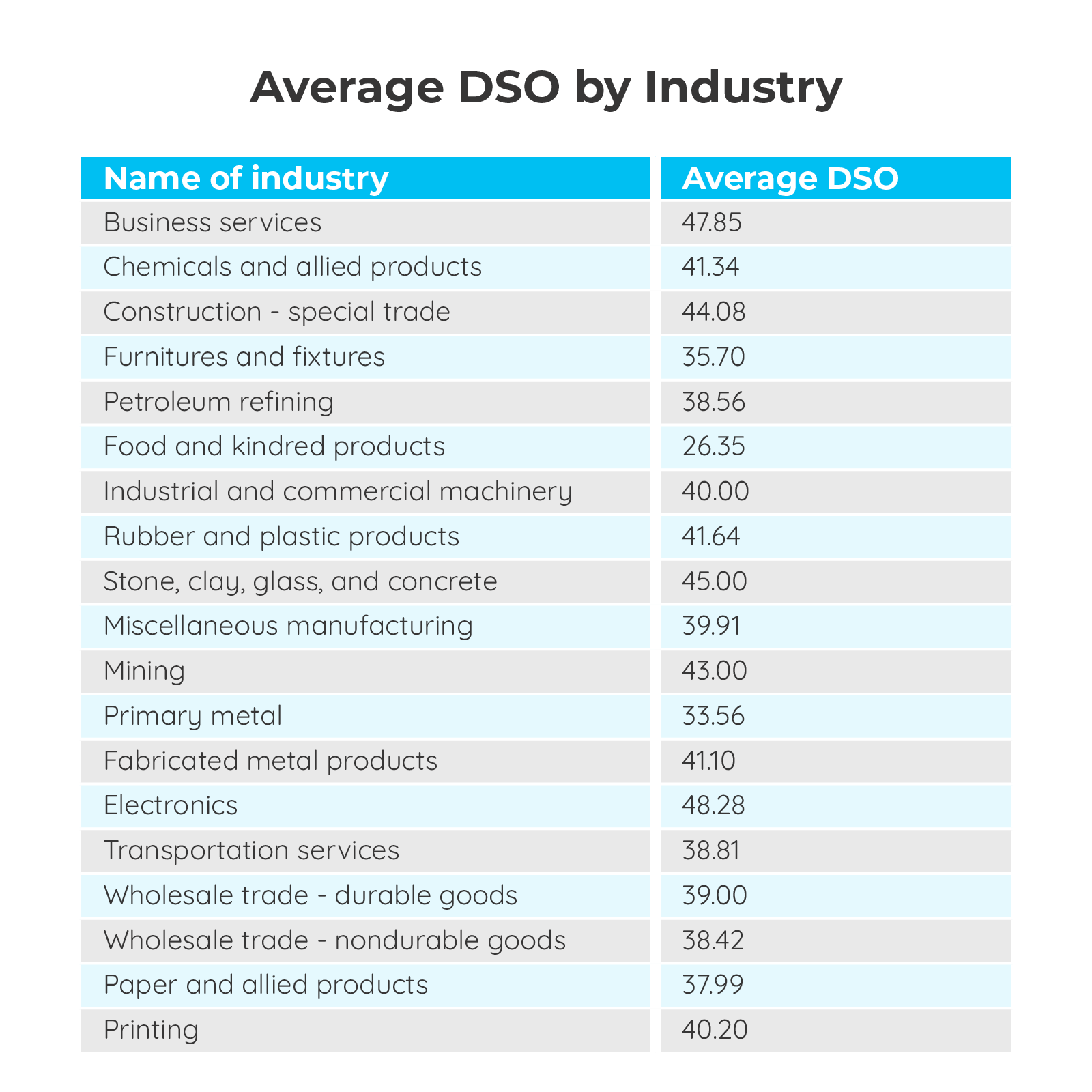

There is not a single DSO number that represents excellent or poor accounts receivable management, since this number varies considerably by industry and by the underlying payment terms. On average, any number below 40 is typically considered a "good" number. But if we look at different industries, recent numbers suggest that in the pharmaceuticals space, DSO is 62 days whereas in textiles, apparel and footwear it's 98 days, and in grocery and specialty retail, it’s only 7 days. So clearly, business models and payment options matter.

Generally speaking, however, a lower ratio is more favorable because it means companies collect cash earlier from customers and can use this cash for other operations. It also shows that the accounts receivables are good and won’t be written off as bad debts.

A higher ratio may indicate a company with poor collection procedures and customers who are unable or unwilling to pay for their purchases. Companies with high days sales ratios are unable to convert sales into cash as quickly as firms with lower ratios.

How do I improve my DSO?

A high DSO can have a number of causes, ranging from inefficient collection practices to a convoluted payment process.

A simple first step toward reducing DSO is to ensure that your payment process is simple and customer-friendly. That means providing features such as a self-service payment portal that allows customers to make payments at their convenience as opposed to during your business’s operating hours.

Ideally, the payment portal should also allow customers to make payments in their preferred method — be it credit card, ACH, or wire transfer — and facilitate things like cross-border payments in their preferred currency. Put simply, the easier you make it for your customers to make payments, the more likely they are to pay in a prompt manner.

Timely delivery of invoices and regular follow-up until payment is received are also essential aspects of reducing late payments. To accomplish this, it helps to have an automated system that not only immediately sends invoices to customers but also provides customizable workflows for regular follow-up that help keep payment top-of-mind.

Adopting AR software that utilizes predictive analytics powered by artificial intelligence (AI) and machine learning is another key method of reducing DSO. By using algorithms, past customer payment behavior is assessed, and predictions are made about which invoice invoices your team can expect to be paid late, and when they are likely to be paid. This allows your team to prioritize high-risk accounts, helping prevent late payments before they become a problem.

Challenges with DSO

DSO has its place in providing an overview to business health and processes. However, there are some issues with the metric to keep in mind, as it’s not always the best number to represent business efficiency or profitability.

Seasonality: DSO is a linear metric, meaning it uses numbers over time against a total. It's the law of averages. However, in seasonal industries, it's best to compare prior year’s months or quarters with current year's to accommodate the dips and bumps in cash flow. Think about businesses heavily reliant on summer tourist seasons, or special retailers whose revenues spike in line with specific holidays.

Sales complexity: While DSO can be a leading indicator, the complexity of the business' sales offers, the types of promotions being run and the credit being extended all impact gross revenue, which is part of the equation. However, complex credit terms or an influx of high-risk customers due to a marketing promotion, can skew the real picture of what’s happening with your business.

These challenges can be addressed with calculated adjustments, which means DSO can still be a valuable "weathervane" metric for any business that gives it some thought.

What KPIs should I track in addition to DSO?

Because of the limitations of DSO, it helps to track additional KPIs that will help you measure your organization's financial health. Below are nine additional KPIs that you should regularly calculate.

Cash Conversion Cycle – the number of days required to sell inventory, collect receivables, and pay bills without penalties.

Working capital – the difference between a company's current assets and current liabilities.

Cash Asset Ratio – a ratio used to determine a company's liquidity by assessing its ability to pay off short-term obligations with cash and cash equivalents.

Past Due A/R – the amount of accounts receivable collected after its due date.

Aging buckets – a way of categorizing past due invoices based on how far past their due date they have gone, e.g., 0-30 days, 31-60, 61-90, and over 90 days.

Collection Effectiveness Index – a way of measuring what was owed to a company versus what was collected over a given time period.

Accounts Receivable Turnover – a ratio that measures how effective a company is at collecting debt and extending credit.

Bad debt write-offs – the amount of debt written off when an invoice is determined to be uncollectable.

Cost of credit – the amount of money an organization pays the bank for running the business on a trade credit model.

Nicole Dwyer

SVP, Digital Americas

Nicole Dwyer is the Senior Vice President, Digital Americas at Quadient, leading the region’s digital strategy, customer experience, and commercial execution. Nicole joined Quadient through the acquisition of YayPay, where she served as Chief Product Officer. She brings deep expertise in payments, product strategy, and regulated industries, with prior leadership roles at Bottomline Technologies, Billtrust, and Fidelity Investments. Recognized for building high‑performing, customer‑centric teams, Nicole aligns strategy and execution to drive digital transformation and operational excellence. She holds a Bachelor’s degree in Management Engineering from Worcester Polytechnic Institute.

Related Content

Discover the latest articles, guides, case studies, and industry updates to help you stay ahead of changing customer expectations, emerging technologies, and market trends.

Time to be remarkable and BE MORE

Quadient Connects brought together hundreds of tech pioneers and business professionals from across the globe, all intent on striving to BE MORE. With 60+ sessions and demos, over 40 digital transformation experts, and a wealth of resources available, participants were at the right launchpad to achieve “more.”

The Collection Effectiveness Index (CEI): What is it & Why is it Important?

We take a look at what the collections effectiveness index is, why it matters, and how you calculate it and improve your overall AR collection efficiency.

A Day In The Life Of An Accounts Receivable Specialist

Click here and read up on what a typical day in the life of an AR specialist might look like. What stage of automation are you at? Contact us to learn more!