Introduction

Ever feel like your profits look good on paper, but your bank account tells a different story? That’s where cash flow comes in. Cash flow tracks the money coming into your business and the money going out. A cash flow calculator makes this easy by showing your net cash flow, in other words, how much cash you gained or lost over a period. This article explains how the calculator works, how to use it, and why regular cash flow tracking helps protect liquidity and support smarter financial decisions.

What is a cash flow calculator?

A cash flow calculator estimates your net cash flow by subtracting total cash outflows from total cash inflows over a set time period.

Business owners, analysts, and controllers use it to:

- Check short-term financial health: See whether your business is cash-flow positive or negative.

- Monitor liquidity and cash runway: Know how much cash you have on hand and how long it will last at your current spending level.

- Manage accounts receivable (AR) and accounts payable (AP) timing: Make sure customer payments come in fast enough to cover the bills you need to pay.

- Support budgeting and forecasting: Plan ahead for upcoming expenses, sales changes, and cash gaps.

- Make better decisions about loans, repayments, and investment: Understand what your business can realistically afford.

In plain terms, it tells you whether you’re cash-flow positive or negative, and how quickly things could change.

Why this matters (more than you think)

Cash flow is often the real deciding factor in whether a company can stay stable, and should be your primary focus from a financial perspective.

For example:

- You might close a strong month in revenue, and still have low cash. If your customers are slow to pay their invoices, your situation could be dangerous.

- You might have good profit on paper, but still struggle to make payroll because of large upfront expenses.

- You might have a growing company and still face cash crunch (more inventory, more staff, more costs).

A cash flow calculator quickly makes the situation visible and clear. It's a powerful tool for any business.

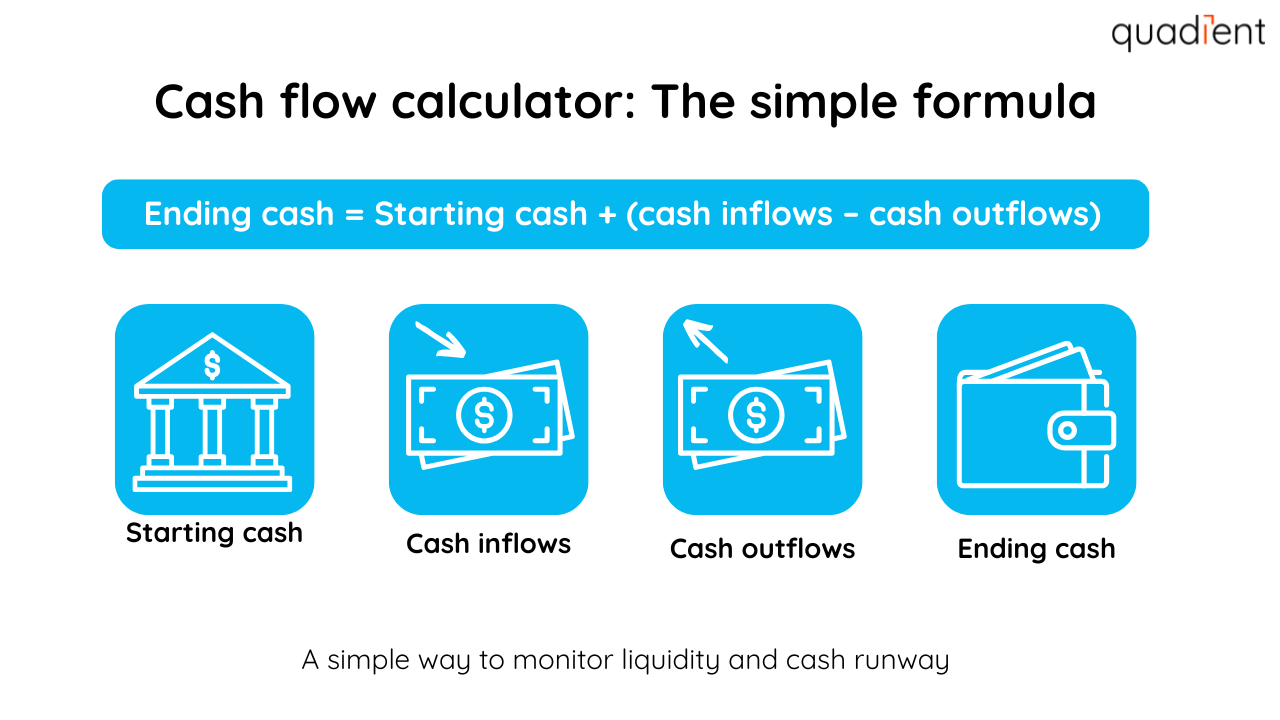

How a cash flow calculator works

Most cash flow calculators use the same core formula:

Cash at end of period = starting cash + (total cash inflows – total cash outflows)

This formula shows whether your business generated more cash than it spent during the period.

- Starting cash: The cash you have at the beginning of the time period you’re measuring.

- Cash inflows: All money coming into your business during that period.

- Cash outflows: All money going out of your business during that period.

- Ending cash: The cash you have left after the period ends.

How to calculate cash flow step by step

Step 1 – Enter starting cash

What to include:

- Cash in business current accounts

- Cash in business savings accounts

- Petty cash

- Cash equivalents you can access immediately

What NOT to include:

- Unpaid invoices (accounts receivable)

- Inventory

- Equipment value

- Credit card limits

Those items matter for financial reporting, but they aren't cash. And a cash flow calculator is about cash.

Step 2 – Add cash inflows

What to include:

- Customer payments

- Sales revenue

- Paid invoices

- Loan funding

- Investment deposits

Tip: For many businesses, the biggest inflow is customer payments. That’s why invoice timing and payment speed are so important. A company can be doing great work and still run into cash trouble if customers consistently pay late.

Think of it like your personal budget. Your salary or wages are an inflow, and your rent and grocery bills are outflows. A cash flow calculator works the same way, just for your business.

Step 3 – Input cash outflows

What to include:

- Payroll

- Rent

- Insurance

- Taxes

- Vendor bills

- Loan repayments

- Capital expenditures (equipment, vehicles, upgrades)

A helpful way to think about cash outflows is to group them into two types:

- Fixed outflows (usually stable month to month)

- Rent

- Payroll

- Insurance

- Subscriptions

- Variable outflows (change depending on volume or season)

- Inventory purchases

- Shipping

- Marketing spend

- Contractor costs

- Repairs and maintenance

This makes it easier to identify where you have control when cash is tight.

Step 4 – Calculate and review

Once you enter the numbers, the calculator shows:

- Net cash flow (inflows minus outflows)

- Ending cash balance

This gives you a snapshot of liquidity, so you can spot issues early.

If the ending cash number looks tight, that’s your cue to dig deeper before the next payroll run or big supplier payment hits.

How to interpret the result

The calculator output is simple, but what you do with it is where the value really is.

Here’s what the result usually tells you:

- Positive net cash flow: Operations are likely stable for this period

- Negative net cash flow: You may need to act quickly

- Low ending cash balance: Even if net cash flow is positive, you could still be at risk

That last point surprises a lot of people. If your starting cash was low, even a positive month may not leave you with enough buffer.

Example: Calculating business cash flow

Here’s a simplified example for one month:

Category | Amount |

|---|---|

Starting cash | £10,000 |

Total cash inflows | £18,000 |

Total cash outflows | £15,500 |

Net cash flow | £2,500 |

Ending cash | £12,500 |

What this tells you: The business generated positive cash flow. That usually means operations are stable and the company can cover short-term costs without scrambling.

What a controller or analyst would notice

This is where finance teams start asking the questions that keep businesses out of trouble.

A financial analyst or controller would also ask:

- Are inflows stable month to month?

- Are outflows predictable?

- Is the ending cash balance enough to cover next month’s obligations?

- How much of the inflow is recurring vs. one-time (like a loan)?

- Are loan repayments increasing in the next quarter?

This is why cash flow calculations are not just “accounting tasks.” They are short-term decision tools.

What is a cash flow calculator used for?

A cash flow calculator is useful for more than just tracking cash. It supports real decisions.

Business planning and forecasting

Cash flow calculators help forecast upcoming expenses, sales, and investment needs, and identify potential cash gaps or surpluses.

For example, you might forecast:

- A slower sales month after a seasonal peak

- A large equipment purchase in 6 weeks

- A tax payment coming due

- A staffing increase

Once you have a good forecasting system in place for your cash flow, you will be in a much better position to anticipate any of these events.

Loan and debt management

Debt can be useful as long as cash flow supports it.

A cash flow calculator helps you to understand your repayment capacity by answering simple questions such as:

- Can we actually afford a £1,200 monthly loan payment?

- What happens if sales drop by 15% in a month?

- Do we have enough cash buffer for two months of repayments?

These calculators can also help you when you're considering to take a loan.

Investment evaluation

Cash flow calculators help you evaluate investments by estimating:

- How much cash goes out upfront

- When cash returns are expected

- Whether the investment causes short-term liquidity risk

Example: You might invest £20,000 in new equipment. It could increase production and revenue, but if that £20,000 drains your cash and leaves you unable to cover payroll, the timing could hurt you.

Risk and liquidity management

Cash flow is one of the clearest indicators of short-term risk.

A calculator helps you see:

- If you’re approaching a cash shortage

- If you have enough buffer for emergencies

- Whether your business can handle delayed customer payments

Even healthy businesses face risk when cash is tight. A single delayed invoice can create a chain reaction, especially for small companies.

Personal or small business budgeting

Freelancers and small businesses often use the same approach each month to control spending and prevent cash shortfalls.

For example:

- A freelancer may have uneven inflows depending on client work.

- A small retailer may see inflows spike in one season and drop in another.

- A contractor may have large upfront outflows for materials.

A simple cash flow calculator helps avoid “surprise” low-cash months.

Why calculating cash flow matters

Cash flow is a practical financial metric for small businesses and finance teams.

Positive cash flow supports stability

Positive net cash flow means you can cover daily operations, pay bills, and reinvest in growth.

It also means you can:

- Hire when the time is right

- Buy inventory without stress

- Pay vendors on time (often earning better terms)

- Build a cash reserve

Negative cash flow is a warning sign

Negative cash flow may mean your business is at risk of falling behind on payroll, vendor invoices, or loan repayments. It can be a warning sign, but it doesn’t always mean your business is failing. It might just be a temporary crunch. The key is spotting it early so you can act.

Operational viability

Cash flow ensures suppliers, employees, and taxes are paid on time. Even profitable businesses can fail if they run out of cash.

This is why people say, "Profit is an opinion." Cash is a fact.

Financial health assessment

Cash flow provides an at-a-glance view of liquidity and sustainability, especially when revenue is tied up in unpaid invoices.

This is one reason financial professionals often track:

- Days sales outstanding (DSO)

- Average invoice payment time

- Overdue invoice volume

- Cash conversion cycle

Those metrics directly reflect how quickly cash arrives.

Strategic decision-making

Cash flow data helps you decide whether to expand, hire, invest, or hold back.

A cash flow calculator supports decisions like:

- “Can we afford to hire a new person next month?”

- “Should we expand now or wait until Q3?”

- “Can we take on a large project without financing?”

Debt and risk management

Understanding cash flow helps businesses stay ahead of liabilities and avoid overextension.

It also reduces stress. When you know your cash position, you stop making decisions based on fear or guesswork.

How do I calculate a cash flow statement?

To calculate a cash flow statement, you categorise cash into operating, investing, and financing activities and total each section.

A typical cash flow statement includes:

- Operating cash flow (cash from core business activity)

- Investing cash flow (cash used for assets and investments)

- Financing cash flow (cash from loans, repayments, and funding)

Learn more here: Cash flow statements.

What are the five rules of cash flow?

There are many “rules,” but these five are practical and easy to apply:

- Know and understand your cash position on a weekly basis

Even if you report monthly, having a weekly awareness of your cash flow will give you a much better overview. - Treat invoices like cash only once they've been paid

Revenue becomes cash when money hits your account. - Match payment timing with your cash flow timing

Only pay bills in the same rhythm as your cash flow comes in. - Build a cash buffer before you need it

A reserve reduces panic and helps avoid poor financing decisions. - Use cash flow trends, not single months

One month can be unusual. Trends tell the real story.

These five rules help small businesses stay stable even when sales fluctuate.

How often should you calculate cash flow?

For most businesses, it’s smart to calculate cash flow:

- Monthly, as a baseline

- Quarterly, for higher-level reporting and planning

- Weekly, if your business is seasonal, fast-growing, or cash-sensitive

If you’re monitoring short-term cash health, more frequent reviews give you more control.

Conclusion

Cash flow is one of the clearest signals of short-term business health. A cash flow calculator helps you quickly see whether you have enough money coming in to cover what needs to go out, so you can plan ahead and avoid surprises.

If you want to improve cash flow over time, the next step is often to accelerate collections and reduce manual work. Learn how Quadient can help: Accounts receivable automation.

Calculate your business cash flow in minutes, then strengthen your liquidity with smarter AR processes.