Introduction

Understanding the difference between accrued expenses and accounts payable (AP) is key to getting your financial reporting, budgeting, and cash flow right. While both fall under short-term liabilities, they’re handled differently and show up at different times. For AP teams, recognizing how they differ is critical to closing the books accurately and staying audit-ready.

In this article, we’ll clear up the confusion. We'll cover the core differences, clarify common misconceptions, and demonstrate how automation tools like Quadient AP Automation can make managing both tasks easier, boost visibility, and reduce manual work.

What are accrued expenses?

Accrued expenses are costs that a company has incurred but hasn’t yet been invoiced for. These are typically recognized at the end of an accounting period to match the expense with the revenue it helped generate, a standard practice in accrual-based accounting.

Key trait: Although there’s no invoice yet, the business still owes the money.

Typically, accrued expenses are recorded through an adjusting entry at the end of the accounting period. These entries ensure that costs, such as interest expense, utility costs, or wage expenses, are reflected in the correct period, even if an invoice has not yet been received.

Common examples of accrued expenses

Employee wages earned but not yet paid

Utilities used but not yet billed

Interest on loans accumulating daily

Taxes owed at the month or year-end

Example: A company uses electricity throughout the month but doesn’t receive its electric bill until the following month. The expense is accrued in the current month to match the usage.

What are accrued liabilities?

Accrued liabilities are a broader category on the balance sheet that encompasses accrued expenses and other similar items. They represent all obligations that have been incurred but not yet paid, whether or not they’re traditional operating expenses.

These amounts are recorded in a liability account in the balance sheet, such as "Accrued expenses payable" or "Interest payable," depending on the type of obligation. They may include items such as accumulated expenses, estimated amounts, and unpaid loan interest.

Think of them as the umbrella; accrued expenses are one type of expense.

What is accounts payable?

Accounts payable refers to funds that are owed to vendors for goods or services that have been received and invoiced. It’s one of the most familiar types of current liabilities, tracked on the balance sheet.

Key trait: An invoice has been received and entered into the general ledger.

Examples of accounts payable

Vendor invoices for office supplies

Inventory purchases on credit

Software subscriptions are billed monthly

Example: Your business receives a $2,500 invoice from a supplier on June 15 for materials delivered. The invoice is recorded in AP and scheduled for payment within 30 days.

How the AP process works

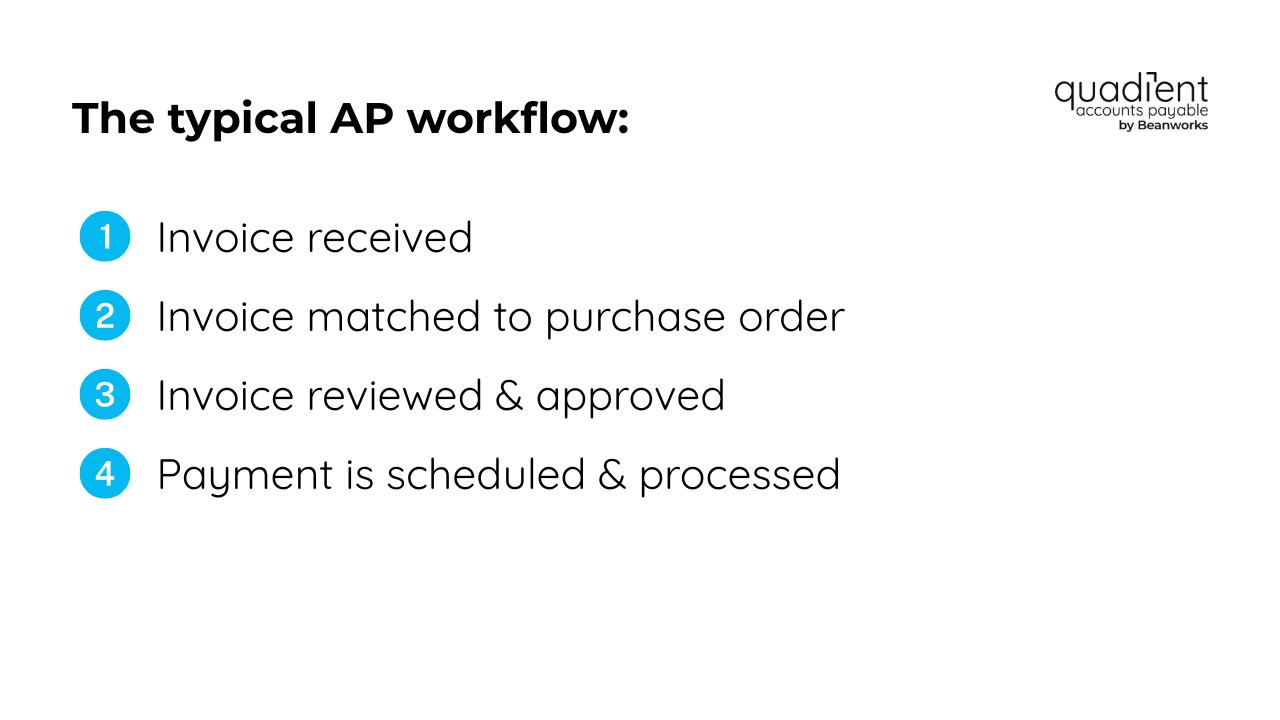

The typical AP workflow looks like this:

Invoice is received

Invoice is matched to a purchase order (PO)

The invoice is reviewed and approved

Payment is scheduled and processed

A typical invoice processing system includes three-way matching, vendor communication, and tracking of early payment discounts to optimize cash flow. This ensures clean accounting records, improves financial statement accuracy, and strengthens AP management.

This process helps keep vendor relationships solid, prevents late fees, and ensures your cash flow forecasts stay on point.

Accrued expenses vs accounts payable: Key differences

Feature | Accrued expenses | Accounts payable |

|---|---|---|

Recognition timing | Incurred but not yet invoiced | Invoice received but not yet paid |

Source documentation | Based on an internal estimate | Based on the vendor invoice |

Financial reporting | Adjusts the income statement and liabilities | Shows up as AP on the balance sheet |

Control mechanism | Typically handled by accounting | Managed by the AP department |

Recognition timing

Accrued expenses are recognized when the expense is incurred, regardless of whether an invoice has been received. This ensures the financials reflect the actual cost of doing business in a given period. In contrast, accounts payable only appear once an invoice has been received and logged into the system, which may occur after the service or product has been delivered.

Source documentation

Since there’s no invoice for accrued expenses, finance teams have to estimate what’s owed based on internal data or past usage. With accounts payable, the amount is clearly stated on a vendor’s invoice.

Financial reporting

Accrued expenses impact both the income statement and the balance sheet, as they increase liabilities and recognize costs in the correct accounting period. Accounts payable, meanwhile, are only listed on the balance sheet as liabilities and don’t affect the income statement until paid or accrued through an expense entry.

Control mechanism

Accruals are often managed by the accounting team, who make manual or automated entries during the month-end close. Accounts payable typically run through the AP department, following a clear process, from receiving the invoice to approving and issuing payment. This helps keep internal controls tight and responsibilities clear.

Example: A company receives cleaning services in March, but the invoice doesn’t arrive until April. When closing the March books, the company accrues the expense, even though the invoice hasn’t been received.

If the invoice had been received in March, the cost would fall under accounts payable.

Why understanding the difference matters

Distinguishing between accrued expenses and accounts payable directly impacts the accuracy of your financial reporting. When liabilities are correctly classified, profit and loss statements reflect actual costs, and keeps the balance sheet clean and reliable. It also affects liquidity metrics—such as the acid-test ratio—which rely on a clear picture of short-term assets and liabilities.

Getting it right is also important when it comes to remaining compliant with regulations. Standards like GAAP and SOX require clear documentation and proper accounting practices, especially during audits. Misclassified expenses can raise red flags and slow the audit down.

From a strategic standpoint, the distinction affects forecasting. If liabilities are entered into the wrong period or category, cash flow models and budgets become distorted, making it more challenging to plan and allocate resources effectively.

Clarity also improves decision-making. Accurate, timely data enables better vendor negotiations, strengthens internal controls, and helps teams close the books faster and with greater confidence.

How AP automation can help

Manual processes in accounts payable often create bottlenecks, delays, and errors—issues explored in detail here. These challenges cost time and money, but automation can solve them.

Simplifying the AP workflow

Tools like Quadient AP Automation streamline every step:

Smart routing and approvals

Integrated vendor payment workflows

Real-time accrual visibility

With advanced dashboards, teams can track both payables and accruals across departments. No more spreadsheet wrangling or missed liabilities.

Reducing manual errors

Automation means fewer missed entries, fewer duplicate payments, and stronger internal controls over expense recognition.

Quadient in action

Finance teams using Quadient report faster period closes, greater accuracy in accruals, and improved compliance.

Want to see how Quadient compares to other options? Check out our comprehensive review of the best AP automation tools to compare features, pricing, and more.

Conclusion

Accrued expenses and accounts payable are both short-term liabilities, but they aren't the same. The key differences come down to timing, documentation, and the way they impact the books. Accrued expenses are recorded even without an invoice. Accounts payable, on the other hand, are linked to invoices that have been received but not paid. Knowing the difference is critical for accurate reporting, staying compliant, and making reliable forecasts.

Tools like Quadient AP Automation simplify this by improving visibility, reducing errors, and streamlining the entire payables process.

Ready to simplify your AP process? Explore Quadient AP Automation or request a demo today.